One of the benefits of marrying young is that Michael and I never had much of an opportunity to surprise each other with finances. We started dating before I was legally able to hold a job, and our bank accounts have been linked in some way or another since I was eighteen. So by the time I graduated college and was staring down my first student loan payment, we’d had plenty of time to reconcile the very, very, very large number on the bill.

Sometimes I forget that massive student loan debt is somewhat of a uniquely millennial problem. For me, it’s always felt like a foregone conclusion. College is expensive, we didn’t have the money to pay for it, and that means you get slapped with loans. A+B=College loans or bust.

But it wasn’t until I started talking with Meg about our respective years at NYU (currently one of the worst schools in the country in terms of both cost and student loan debt), that I was made aware of just how much the game had changed in the six short years between when she went to school and when I did. It’s a particularly interesting case study, since Meg was technically born the last year before the millennial generation started. So even though, day to day, we act and look like the same generation, our financial histories are different simply because of the generational math of when we happened to be born.

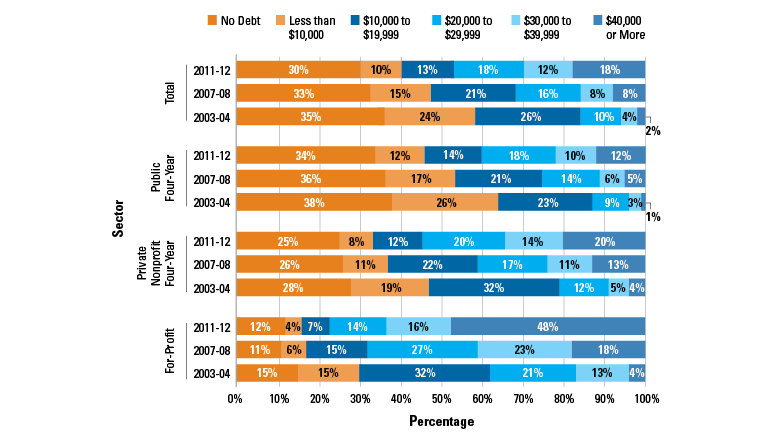

Let’s do some numbers, shall we? Between the year that Meg graduated and the year I graduated, a four-year degree at NYU had increased in cost by 11%. But since Meg graduated and now? It has risen from an inflation adjusted amount of $48,000 per year to over $75,000. Not a typo. $75,000. A year. But that’s not the only problem. As tuition skyrocketed, the percentage of the tuition that private four-year schools offered in scholarship money held essentially flat. (Worse, the proportional scholarship numbers at four-year public schools actually got worse.) Which means you end up with student loan debt figures like this one from CollegeBoard:

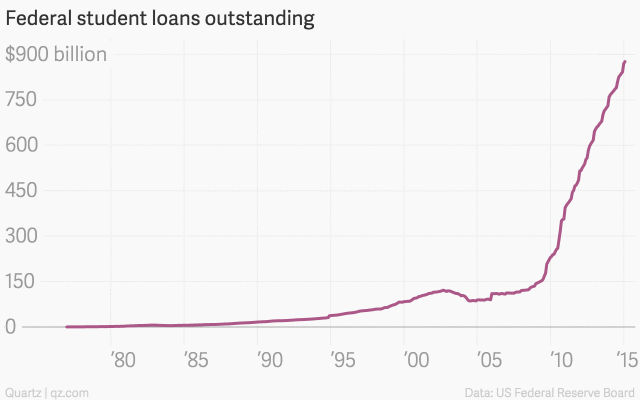

And granted, while NYU is one of the most expensive schools in the nation, it’s certainly a symptom of a much bigger problem. You can see how these numbers play out nationally in charts like this one, from qz.com. (Don’t even look at student loan debt delinquency charts if you want to sleep at night.)

So let’s say you’re lucky enough to have parents who can contribute $20,ooo per year to your tuition. Assuming the rest is made up in student loans, the difference between Meg’s debt and yours (inflation adjusted) would be $20,000 vs. $55,000, per year.

Which means that, within a generation, student loans have morphed from a manageable expense (the kind that baby boomers love to tell us you can pay off by mowing lawns over the summer) into a financial beast with very sharp teeth. This phenomenon has, of course, been talked into the ground. But what we haven’t discussed is what this phenomenon does to a marriage. Because there is no way six-figure debt (which doubles if you marry someone with their own debt) isn’t going to put some kind of strain on a marriage. So I polled some friends to see how they were managing things. And while most of us graduated before the crazy post-recession tuition hikes, the answers still varied across the board:

One person said they paid off student loans together, but kept the actual debt separate, while merging all other finances:

In our household, while we have significant student loan debt, it’s not enough to feel like we’re drowning in it (at least in relation to our incomes), which makes us feel super lucky. The break down is this: I paid off my student loan debt before we got married, and my partner has grad school loan debt. Since we have joint finances, we pay the monthly payment together, no questions asked. However, when it came to paying down the loan faster, my deal with my partner is that he needed to pick up part-time work to do that. I wasn’t going to put things like my bonuses toward his student loans. Mostly, this was because I had paid off my undergrad loans on my own, and his parents had paid for his undergrad in full, so he’d never had to pay off loans. I felt like he needed the experience in working on paying off loans (faster) on his own. It’s worked out well. While we feel jointly responsible for the loan payments, he has a lot of pride in watching the number shrink.

Also, I should note that because federal student loans attach to the student alone (they are not marital property), I refused to refinance the loans in a way that would attach to me. I’m happy to help pay them off, but if my partner died or we got divorced, I wouldn’t want to be responsible for them.

While another kept their loans totally separate:

My husband and I both have a big chunk of student loan debt and we pay our own loans separately. We’ve discussed pooling our resources and aggressively attacking our student loans one at a time to pay them off faster, but we haven’t put anything in place to make that happen. We still kind of operate as two individuals who split the joint expenses. Also our other financial goals are taking precedence over our student loans, like saving for retirement and for a house. I would like to see us prioritize paying them off or paying them down significantly in the near future.

One talked about the stress that different styles of handling debt can produce:

Today student loans are a non-issue in our marriage: we both have minimal monthly payments (thanks to early ’00s schooling) with low interest rates and neither of us prioritize paying them off sooner than we’re scheduled to. BUT. When we were very early into our dating days, I found out my partner hadn’t been paying his loans for around three years because he was making cash money, and like… dropped off the grid? Once he got a real job, the loan people found him and threatened to garnish his wages if he didn’t immediately pay $800—which was about as much as the vacation we were supposed to go on the very next day cost. My uber responsible loan-paying self had a meltdown in a public place when I found this all out, but to his immense credit, he quietly sorted it all out, hustled the money up from somewhere, AND still paid for his half of the vacation. Oh, and hasn’t missed a payment since.

And then there’s the outlook that most closely resembles my own:

Student loan debt was something that happened for us before we even realized the extent of its ramifications. We now have a ton of it, and no real clue when or if it will ever be paid off. We haven’t had this impact us negatively in any real, big picture kind of way, but we’ve also never tried to buy a house or an expensive car. Our student loan debt even kind of feels like pretend debt, the same way it felt like pretend money when we first received it.

As for me, if I were to get married now, I’d hate for my student loan debt to be counted against me. Taking on my loans was a decision I made when I was a child, before I had any idea what nearly six figures of debt would do to my life. But on the flip side, should we have take responsibility for the financial decisions our partners made alone, before there was a partnership to consider?

But beyond the personal implications, my concern for the rising costs of a four-year education is of the bigger picture: As tuition increases skyrocket, what is student loan debt going to do to the thing we think of as “marriage” moving forward? Because massive debt starts a ripple. We’re already getting married later, having kids later, buying homes later. What happens when you add (two) six-figure repayments to that mix?

Do you or your partner have student loans? How have they impacted your relationship?

*Tuition sources: NYU.edu via the Wayback Machine